The storm that began in the U.S. five years ago, swept governments, banks and mortgage financiers.

The outbreak of the subprime mortgage crisis in the U.S. arrives to its fifth year with a legacy that includes a global economic crisis that seems endless: the almost certain breakdown of the euro, and in the case of Greece, Spain, and most likely France, Portugal and Italy , among others, the need to seek bailouts from the European Union.

After five years, Greece is no longer owned by its people, but by bankers. The country experienced a total collapse since the alarm bells went off on August 9, 2008. The same has happened to Spain, that went from a growth rate of 4% to a negative one which is expected to be 1.5% in 2012. As it happened in other sovereign debt stricken countries, Spain lost half of its stock market value — not that it really means anything in the real world — and corporate profits, depending on who you ask, have seen dramatic losses or dramatic gains.

Almost all Euro zone countries have seen their ability to request loans erased or deeply eroded, given their loss of reputation as trustworthy borrowers. That fact has also made it more expensive for nations to pay for the already existing debt, which turned attention to their leaders. In response to the fiscal challenge, governments simply decided to continue business as usual, that is, borrowing more money at higher interest rates, in order to finance the gigantic welfare systems they do proudly own. Through the years, the deficit has grown, and so has the debt and the interests on it. The sovereign debt bubble, to use a familiar term, is that much closer to burst, given countries like Spain’s inability to make the payment on its debt, while continue to borrow.

The negative of the European governments to act in accordance with the best interests of their people, resulted in more unemployment, more debt, less production, and less sovereignty. In the Euro zone, most countries have been downgraded by the banker created rating agencies, such as Fitch and Moody’s which resulted in the increase of borrowing costs.

The risk premium, index of investor confidence in the sovereign debt of a country is measured by the spread between ten-year national bond and the German for the same period, went from complete anonymity to becoming the essential indicator for all economies. In August 2007 the risk premium of Spain, for example, which is the measure of the extra costs demanded by investors for buying Spanish sovereign debt compared to Germany, was 12 basis points, compared to the 630 points it has now.

Even though the subprime crisis was rooted in the United States, where all kinds of schemes were created to defraud borrowers, lenders, families and investment funds, the shock waves rapidly arrived in Europe, where big banks had invested themselves — knowingly and otherwise — in the same fraudulent financial products stained with the subprime lending scam. One of the triggers of the crisis in Europe was the temporary suspension of the liquid value of three funds owned by BNP Paribas on August 9, 2007. This move was a direct consequence of the subprime mortgage debacle in the U.S., where investing firms used customer money to gamble, while their risk was minimum. From every $100 that was put at risk, $97 belonged to pension funds, credit unions , retirement accounts and average investors. Only $3 came out of the pockets of those who risked their customers’ assets.

In most cases, unregulated U.S. financial institutions diversified the risks of subprime mortgage loans through securitization, transferring them to other banks in the credit derivatives market. Derivatives are themselves a form of artificially created ‘financial products’ with little or no value. The lack of transparency and little clarity in the terms of the derivative contracts make this financial instrument the most attractive, but also the riskiest one. In the case of the crisis of 2008, investors only got to know the risk and not the promised high returns in their investments. That is how many individuals, companies and organizations saw their monies simply disappear. Someone had simply ran away with their money.

The supposed harmless securitizations involved the transformation of an asset or a non-negotiable right to payment (eg. a mortgage) into homogeneous debt securities or bonds, standardized and open to negotiation on organized securities markets. Financial institutions took on the risk for two reasons. First, because it was not their money the one at risk, but that of investors. Second, because they knew that government would come to the rescue, as it has now happened. The immediate impossibility to know the total value of these toxic assets and who was exposed to them launched even worse tsunami waves that deepened the crisis to levels never seen before.

The contagion in financial markets collapsed and worked as the perfect excuse for the European Central Bank (ECB), U.S. Federal Reserve and other central banks to take initiate the largest transfer of wealth ever seen in history. Not only had the banks ran away with investors’ money, but they were also about to receive the largest taxpayer funded bailouts ever — which are still ongoing — even though they were the only ones to blame for the collapse of the existing system. Total bailout cash has now reached $1 trillion and this money has mostly been given to selected people in governments as well as international banking institutions. It is important to note that some calculations set the fraudulent derivative market value at $1 quadrillion.

Right at the beginning of the crisis, and in one transaction alone, the European Central Bank gave away 94.841 million euros, one third more than the 69,300 million euros injected on 12 September 2001, a day after the attacks in New York. This move meant little or nothing as the connections in a globalized economy began to reveal that the problems were just about to get worse. The storm started by some U.S. mortgage financing firms became a gale that has so far crushed governments like Greece, Italy and France, mortgage financing giants Fannie Mae and Freddie Mac and investment banks like Bear Stearns and Wall Street’s Lehman Brothers. Those two banks along with many others were literally absorbed and digested by bigger banks, that with taxpayer money, healed all losses they would have and still were left with much more cash to pay fat bonuses to their corporate leaders.

The crisis has gotten to a point where it has mathematically bankrupted almost all if not all developed countries — even though their leaders say otherwise — due to the impossibility for those nations to pay off their debts. Their implosion is just a matter of time. With Spain, France and Italy being unable to meet their obligations and not willing to seek sane fiscal and monetary policies, the break up of the Euro zone is all but imminent. As mentioned in previous articles, the length of time that will pass until the full collapse occurs is in the hands of the banking institutions who originally caused the crisis.

The financial crisis of confidence and credit has led to recession after another in the developed world and has slowed the growth in emerging markets like Brazil or China, but mostly has jeopardized the survival of the single European currency. The effects of the crisis remain to be seen in those regions of the world, where their economies have begun to contract already.

AFP – Three years after Iceland’s banks collapsed and the country teetered on the brink, its economy is recovering, proof that governments should let failing lenders go bust and protect taxpayers, analysts say.

The North Atlantic island saw its three biggest banks go belly-up in the October 2008 as its overstretched financial sector collapsed under the weight of the global crisis sparked by the crash of US investment giant Lehman Brothers.

The banks became insolvent within a matter of weeks and Reykjavik was forced to let them fail and seek a $2.25 billion bailout from the International Monetary Fund.

After three years of harsh austerity measures, the country’s economy is now showing signs of health despite the current global financial and economic crisis that has Greece verging on default and other eurozone states under pressure.

“The lesson that could be learned from Iceland’s way of handling its crisis is that it is important to shield taxpayers and government finances from bearing the cost of a financial crisis to the extent possible,” Islandsbanki analyst Jon Bjarki Bentsson told AFP.

“Even if our way of dealing with the crisis was not by choice but due to the inability of the government to support the banks back in 2008 due to their size relative to the economy, this has turned out relatively well for us,” Bentsson said.

Iceland’s banking sector had assets worth 11 times the country’s total gross domestic product (GDP) at their peak.

Nobel Prize-winning US economist Paul Krugman echoed Bentsson.

“Where everyone else bailed out the bankers and made the public pay the price, Iceland let the banks go bust and actually expanded its social safety net,” he wrote in a recent commentary in the New York Times.

“Where everyone else was fixated on trying to placate international investors, Iceland imposed temporary controls on the movement of capital to give itself room to maneuver,” he said.

During a visit to Reykjavik last week, Krugman also said Iceland has the krona to thank for its recovery, warning against the notion that adopting the euro can protect against economic imbalances.

“Iceland’s economic rebound shows the advantages of being outside the euro. This notion that by joining the euro you would be safe would come as news to the Spaniards,” he said, referring to one of the key eurozone states struggling to put its public finances in order.

Iceland’s example cannot be directly compared to the dramatic problems currently seen in Greece or Italy, however.

“The big difference between Greece, Italy, etc at the moment and Iceland back in 2008 is that the latter was a banking crisis caused by the collapse of an oversized banking sector while the former is the result of a sovereign debt crisis that has spilled over into the European banking sector,” Bentsson said.

“In Iceland, the government was actually in a sound position debt-wise before the crisis.”

Iceland’s former prime minister Geir Haarde, in power during the 2008 meltdown and currently facing trial over his handling of the crisis, has insisted his government did the right thing early on by letting the banks fail and making creditors carry the losses.

“We saved the country from going bankrupt,” Haarde, 68, told AFP in an interview in July.

“That is evident if you look at our situation now and you compare it to Ireland or not to mention Greece,” he said, adding that the two debt-wracked EU countries “made mistakes that we did not make … We did not guarantee the external debts of the banking system.”

Like Ireland and Latvia, also rescued by international bailout packages and now in recovery, Iceland implemented strict austerity measures and is now reaping the fruits of its efforts.

So much so that its central bank on Wednesday raised its key interest rate by a quarter point to 4.75 percent, in sharp contrast to most other developed countries which have slashed their borrowing costs amid the current crises.

It said economic growth in the first half of 2011 was 2.5 percent and was forecast to be just over 3.0 percent for the year as a whole.

David Stefansson, a research analyst at Arion Bank, told AFP Iceland hiked its rates because it “is in a different place in the economic (cycle) than other countries.

“The central bank thinks that other central banks in similar circumstances can afford to keep interest rates low, and even lower them, because expected inflation abroad is in general quite (a bit) lower,” he said.

It’s been at least 15 years since I heard calls for people to wake up because the greatest crisis in humanity’s existence was rapidly approaching. Today, as I watch video and photos from London, and previously from Syria, Egypt, the United States and Lybia, I cannot help but think that those who sought to warn us were simply and plainly correct. Perhaps the most surprising fact is that those truth tellers, who were often identified as conspiracy theorists, told us how it would happen and as the break point got closer and closer, they were even able to predict different aspects of the fall with outstanding precision.

Who would have believed 15 years ago that the world would crumble to its knees and would beg for the implementation of tyrannical policies and regimes in order to bring back law and order? I certainly didn’t. Before I began studying history and current events, I thought society would be able to take care of itself and avoid disaster. But the latest video feeds from London and everywhere else clearly show that society is lost in the foggy alternative reality they were born into 50 or more years ago. The social engineers played their hand well and now have most of the population consuming itself in a web of self-degradation, death and perversion fed to us as the sexiest fad for almost half a century.

In England, polls show that upwards of 65 percent of people are now calling for the use of rubber bullets, water canyons, police abuse and other tyrannical practices because they are too afraid to organize with their neighbors and take care of the looters that are destroying decades-old family businesses, homes, cars, shoe and clothing stores and other property to get their hands on the latest electronics, jewelry and various valuable products by breaking windows, smashing store front doors and pulling citizens from the their cars to smash their heads on the streets. Instead, British people are now calling for a government sponsored Police State.

Notice that most of the places that are being affected by riots and unrest are sections of the society whose members are unarmed and who cannot defend themselves because their government, which cannot protect them 24/7, implemented regulations to ban the people’s right to be armed and to defend their properties and their families. London shows signs of the most recent confrontation between members of the government-dependent underclass and the hard-working middle class, just as the social engineers planned it. As governments cut spending in a failed attempt to fix deficits and reduce their debt, it is exactly the underclass that feels the pinch first. But instead of attacking government policies and the entities responsible for the financial collapse, this uneducated underclass takes it upon themselves to beat the daylights out of middle class folks who suffer from the bank-sponsored self-inflicted financial crisis.

The financial and political apartheid taking place in the world -where governments steal the people’s pension funds to invest them in fictitious financial products, banks get bailed-out as they charge interest rates and / or fees for people to keep money in their accounts, the government cuts social security and medical care spending, people’s paychecks and pension buy less food- will continue to increase social volatility not only in London or Greece, but in the Americas, Asia, Africa and everywhere else. The Social Experiment failed horribly. But then again, it was meant to fail. The divisions meant to occur in order to monopolize, control and conquer arrived right on time.

The underclass as well as the dumbed down middle-class that for centuries sucked off the system through government established dependence programs only woke up after finding themselves with no jobs, no pension, no savings and no future. They woke up from their eternal state of slavery because the bribery scheme known as welfare that the government used to hook them up is suddenly crashing down, and they have not safety net to fall onto. What do I mean by bribery scheme? In 2007, the richest country in the planet had at least 52.6 percent of the people receiving government aid of some sort: pensions, social security and so on.. One in five Americans held a government job or a job that depended on government spending. Around 19 million used food stamps and 2 million got subsidized housing. If that is not government bribery, I don’t know what is it. The social engineers made sure from the start that only two classes existed: the productive class and the parasitical class. Both the government and the dependent classes are equally violent towards those who produce and who support them throughout their lives.

But perhaps one of the most abhorrent aspects of the current societal collapse is that the social engineers point to the underclass and the working class as those responsible for the crisis. That’s right. They accuse the so-called “useless eaters” for their greed and for living beyond their means and hold them responsible for the crisis we now experience. Both the underclass and a large part of the middle class are in part responsible for their greed and decadence. But weren’t they born and bathed into a system that promoted and facilitated their greed, decadence and dependence? Of course they were. Should the underclass and the middle class then be held responsible for the now developing crisis because they were greedy and dependent? Of course not. But that is what the bankers, the social engineers want the dumbed down majority to think, and that is why tonight racial divides grow bigger in London, the United States, Africa and Asia. The underclass believes that the middle class are the ones responsible for the crisis because they are successful business owners and were able to take care of themselves and their families. In the meantime, the bankers who are responsible for both classes’ misery run rampant ripping people off around the world.

The people are to blame, say the bankers, because they want more services but don’t want to pay more taxes. Due to the fact millions have not bought the propaganda, the government is now playing the collectivist card. “There is no need to look for anyone to blame because we must now come together to solve our problems”. Neither the government nor the banks want the taxpayers to fully understand that these two entities are solely responsible for the current state of affairs. Governments have bribed citizens openly for at least a century in order to control them, therefore it is insane to believe that someone will buy the government and bank sponsored propaganda.

While millions of people lose their jobs, homes and lives because they cannot afford them, a few decadent scum bags consume themselves in fake tribalism, racism, theft and violence while the cowardly ones wait for the state to do something and beg for Martial Law and a Police State. Those who accepted the American-created culture of death, sex, thuggery, drug use, suicide and gang oriented behaviours are now acting as what they always dreamed to be: a bunch of disaffected slaves with no jobs or future that look up at rappers, singers, sports figures, electronics, alcohol and drugs to fulfill their empty lives. The world went from praising explorers, scientists, fire fighters, inventors and community leaders to worship ‘bling’ and Madison Avenue-created delusion.

Those who took advantage of a corrupt debt-based system to get their holiday vacation, car and house loans were shocked after the banks that own their livelihoods cut off lines of credit three years ago to put an end to the fantasy reality they were accustomed to for so many years. Those who foolishly believed that paying into the public pension system would guarantee them some devalued change to live the rest of their lives, even though many had warned of its non-existence, were not only fools, but also irreparable willful ignorants. They trusted their government so much to give them everything, that no room was left to think that the same State could one day decided to take it all away; which is what is happening now. So now, the most dependent members of society are blaming other citizens and not the banks and the governments for their misery. Why? Because blame is the base of Statism and the State has shown people well to accept the blame game when it favours the State. They are now begging the social engineers to put an end to their misery. Events like the riots in London and the United States are just the beginning of what is turning out to be a long summer and a coming long winter. Street violence, crime and government opposition will be used by the controllers to take away more of our rights. Government will use armies and violence against peaceful protesters before bringing out austerity and a more visible Police State, to crush people’s right to speak and arm to themselves, track social media, email accounts, and any other sign of dissent.

Now, this is what a broken down society looks like in the developed world. Can you imagine what will it look like in socialist or inherently paternalistic poor countries when austerity, hunger and deep misery gets there?

3M and Cargill are on the list of corporations that asked to be exempted from recently passed laws.

AP

Treasury Secretary Timothy Geithner has decided to let companies continue to trade certain contracts used to guard against swings in currency values outside regulators’ view.

New rules require that many such trades happen more transparently, on exchanges where regulators can see them. But Geithner is exempting certain contracts used by companies to hedge currency rates.

The new financial overhaul law authorized Geithner to carve out such an exemption to stricter regulation.

Business groups argue that tighter oversight of such contracts would be costly and unnecessary. But critics, including some regulators, counter that the whole market for financial contracts called over-the-counter derivatives should face stricter supervision.

The value of derivatives hinges on an underlying investment, such as currencies, stocks or mortgages. Speculators who used over-the-counter derivatives helped fuel the 2008 financial crisis.

Sen. Carl Levin, who pushed for tighter regulation after the crisis, said Geithner’s decision might open the door for lax oversight in the future.

Treasury’s top markets official said the contracts already include many of the safeguards the new rules impose. Investors can find information on the price for each contract, for example. Some of the contracts are traded on electronic platforms, which are less likely to freeze up after an unexpected financial shock.

Imposing new rules would mean “introducing an additional process into what is a very well-functioning market today, and you would be putting more steps into the settlement process,” said Mary Miller, assistant Treasury secretary for financial markets.

Miller argued that even with the exemption, the market will become more transparent. Companies will have to report the contracts in real time, after they make a trade. The information will go to central databanks that regulators can see.

Still, the contracts, called foreign-exchange swaps, wouldn’t be subject to other requirements that experts say would make them more transparent.

The contracts that Geithner carved out account for about $30 trillion of the $600 trillion global market for over-the-counter derivatives, Treasury said. The new, tougher rules will apply to currency swaps, options and other contracts used for similar purposes.

Multinational corporations such as Cargill and 3M argued for the exemption. They said the new rules would have raised their costs, thereby limiting their ability to grow and create jobs.

Advocates of tighter regulation say closer oversight is needed at each stage of the process — before, during and after a trade. They say the exemptions will make some types of trades harder to oversee.

Michael Greenberger, a former official with the Commodity Futures Trading Commission, which is responsible for policing much of the derivatives market, disputed Treasury’s main defense of the exemption — that the contracts expire so fast that they don’t pose serious risks to the financial system.

“Within the next 60 months, there will be a systemic break in this market, said Greenberger, now a law professor at the University of Maryland.

The decision technically is a proposal. Treasury will accept public comments for 30 days before finalizing the exemption.

We’ve been over the numerous BS excuses that US Dollar destroyer extraordinaire Ben Bernanke has made for QE enough times that today I’d rather simply focus on the REAL reason he continues to funnel TRILLIONS of Dollars into the Wall Street Banks.

I’ve written this analysis before. But given the enormity of what it entails, it’s worth repeating. The following paragraphs are the REAL reason Bernanke does what he does no matter what any other media outlet, book, investment expert, or guru tell you.

Bernanke is printing money and funneling it into the Wall Street banks for one reason and one reason only. That reason is: DERIVATIVES.

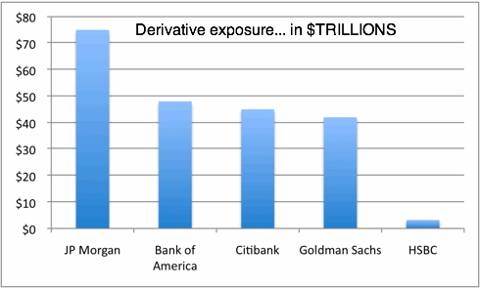

According to the Office of the Comptroller of the Currency’s Quarterly Report on Bank Trading and Derivatives Activities for the Second Quarter 2010 (most recent), the notional value of derivatives held by U.S. commercial banks is around $223.4 TRILLION.

Five banks account for 95% of this. Can you guess which five?

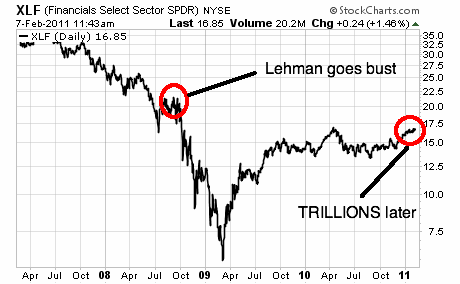

Looks a lot like a list of the banks that Ben Bernanke has focused on bailing out/ backstopping/ funneling cash since the Financial Crisis began, doesn’t it? When you consider the insane level of risk exposure here, you can see why the TRILLIONS he’s funneled into these institutions has failed to bring them even to pre-Lehman bankruptcy levels.

Ben Bernanke is a stooge and a fraud, but he is at least partially honest in his explanations of why he wants to keep printing money. The reason is to try to keep interest rates low. Granted, he’s failing miserably at this, but at least he understands the goal.

Of course, Bernanke tells the public and Congress that the reason we need low interest rates is to support housing prices. He doesn’t mention that $188 TRILLION of the $223 TRILLION in notional value of derivatives sitting on the Big Banks’ balance sheets is related to interest rates.

Yes, $188 TRILLION. That’s thirteen times the US’ entire GDP, and nearly four times WORLD GDP.

Now, of course, not ALL of this money is “at risk,” since the same derivatives can be traded/spread out dozens of ways by different banks as a means of dispersing risk.

However, given the amount of money at stake, if even 4% of this money is “at risk” and 10% of that 4% goes wrong, you’ve wiped out ALL of the equity at the top five banks.

Put another way, Bank of America (BAC), JP Morgan (JPM), Goldman (GS), and Citibank (C) would CEASE to exist.

If you think that I’m making this up or that Bernanke doesn’t know about this, consider that his predecessor, Alan Greenspan, knew as early as 1999 that the derivative market, if forced into the open and through a public clearing house, would “implode” the market. This is DOCUMENTED. And you better believe Greenspan told Bernanke this.

In this light, all of Bernanke’s monetary policies and efforts are focused on doing one thing and one thing only: trying to shore up the overleveraged, derivative-riddled balance sheets of the Too Big to Fails, or Too Bloated to Exist, as I like to call them.

The fact that the bank executives taking this money and using it to pay themselves and their employees record bonuses only confirms that these folks have NO interest in taking care of shareholders or their businesses. They’re just going to take the money and run for as long as this scheme works.

I don’t know when this will come unraveled. But it WILL. At some point the $600+ TRILLION behemoth that is the derivatives market will implode again. When it does, no amount of money printing will save the Too Bloated To Exist banks’ balance sheets.

At that point, it’s game over for Wall Street and the Fed.

Daftar Akun Bandar Togel Resmi dengan Hadiah 4D 10 Juta Tahun 2024

Cara farming gold lebih efisien sekarang mulai populer, simak dulu Result macau. Update kecil kadang punya efek besar di gameplay. Banyak player langsung menyesuaikan strategi.

Togel resmi adalah langkah penting bagi para penggemar togel yang ingin menikmati permainan dengan aman dan terpercaya. Tahun 2024 menawarkan berbagai kesempatan menarik, termasuk hadiah 4D sebesar 10 juta rupiah yang bisa Anda menangkan. Anda perlu mendaftar akun di Daftar Togel yang menawarkan hadiah tersebut. Proses pendaftaran biasanya sederhana dan melibatkan pengisian formulir dengan informasi pribadi Anda serta verifikasi data untuk memastikan keamanan transaksi. Setelah akun Anda selasai terdaftar, Anda dapat berpartisipasi dalam berbagai permainan togel berbagai fitur yang disediakan oleh situs togel terbesar.

Bagi pemain togel yang ingin menikmati diskon terbesar, mendaftar di situs togel online terpercaya adalah langkah yang tepat. Bo Togel Hadiah 2d 200rb tidak hanya memberikan jaminan keamanan dalam bertransaksi, tetapi juga menawarkan berbagai diskon untuk jenis taruhan tertentu. Diskon yang besar ini memungkinkan pemain untuk menghemat lebih banyak dan memasang taruhan dalam jumlah yang lebih banyak. Dengan begitu, peluang untuk mendapatkan hadiah juga semakin tinggi, sekaligus memastikan bahwa setiap taruhan dilakukan di situs yang aman dan resmi.

Update terbaru akhirnya menghadirkan fitur yang lama ditunggu komunitas, penjelasan lengkap menuju bd-innovations.com. Tips rotasi cepat sangat penting di mode battle royale. Salah posisi bisa membuat tim langsung tereliminasi lebih awal.

Update terbaru ini membawa perubahan pada sistem combat yang membuat gameplay terasa lebih dinamis dan menantang baca perubahan lengkapnya pedetogel login. Tips bermain efektif bisa membantu menghemat waktu saat grinding. Fokus pada tujuan utama sangat penting.

Promo isi ulang harian dengan batas klaim terbatas bikin persaingan makin cepat, mekanisme klaimnya bisa kamu cek pada situs toto. Tips penting adalah jaga koneksi internet tetap stabil. Lag sedikit saja bisa mengubah hasil match.

Promo paket hemat ini cocok buat kamu yang mau nabung resource untuk Toto Togel. Sistem daily quest membuat pemain memiliki tujuan setiap hari. Misi kecil ini memberi reward tambahan.

Promo isi ulang sekarang makin menarik karena bisa dapet item pilihan sesuai kebutuhan pada toto slot. Update tampilan karakter bikin visual makin modern. Pemain lama bisa nostalgia sekaligus fresh.

Toto Macau, Pasaran dengan Sistem Pembayaran Fleksibel

Bermain di pasaran yang memiliki kredibilitas tinggi sangat penting dalam dunia togel, dan salah satu yang memenuhi kriteria tersebut adalah Toto Macau. Pasaran ini menawarkan pengalaman bermain yang seru dengan peluang menang yang cukup besar. Selain itu, Toto Macau memiliki sistem pembayaran yang fleksibel, memungkinkan pemain untuk melakukan deposit dan withdraw dengan mudah.

Memilih situs judi online yang tepat sangat penting untuk memastikan pengalaman bermain yang aman dan menguntungkan. Situs Toto hadir dengan berbagai keunggulan, termasuk sistem keamanan berlapis, metode transaksi yang cepat, serta bonus dan promo menarik untuk para pemainnya. Dengan begitu, pemain bisa fokus menikmati permainan tanpa khawatir akan risiko penipuan atau gangguan teknis.

Hiburan sekaligus peluang keuntungan besar bisa didapat melalui toto macau, karena permainan ini menggabungkan sensasi ketegangan dengan kemungkinan memperoleh hadiah berlimpah.

Link Slot Gacor Terpercaya untuk Menang Setiap Hari

Slot gacor hari ini menjadi incaran para pemain Link Slot Gacor yang ingin menikmati peluang jackpot besar hanya dengan menggunakan modal kecil, sehingga mereka bisa merasakan pengalaman bermain yang lebih menyenangkan dan penuh keuntungan.

Event login sederhana tapi worth it ini detail hadiahnya bisa kamu cek lewat toto togel. Komunitas roleplay bikin pengalaman makin unik. Dunia game terasa lebih hidup.

Situs dengan slot Mahjong Ways gacor memberikan jackpot dan Scatter Hitam lebih sering di tahun 2024. Pastikan memilih situs terpercaya yang menyediakan fitur scatter unggulan, sehingga peluang Anda untuk menang lebih besar dan aman.

Dengan Situs Slot Depo 5k, Anda bisa bermain dengan modal kecil namun tetap memiliki kesempatan besar untuk meraih hadiah. Banyak platform judi online kini menawarkan pilihan deposit rendah ini, sehingga pemain dengan budget terbatas tetap bisa menikmati permainan slot favorit mereka. Bermain slot dengan deposit kecil seperti ini tentu memberikan kenyamanan bagi pemain baru maupun veteran.

Situs Slot Gacor Gampang Menang RTP Live Tertinggi

Strategi bermain slot online kini semakin berkembang, terutama dengan munculnya data rtp slot gacor tertinggi. Para pemain dapat memanfaatkan rtp live untuk memilih slot gacor dengan rtp slot yang terbaik, memastikan mereka memiliki peluang menang yang lebih besar. Slot rtp tertinggi yang tersedia hari ini bisa menjadi panduan penting bagi siapa saja yang ingin menikmati permainan yang lebih menguntungkan. Dengan memahami rtp slot online, pemain dapat bermain dengan lebih strategis dan mendapatkan hasil yang lebih memuaskan.

Salah satu hal yang membuat Toto Slot begitu diminati adalah kemudahan dalam bermain. Pemain tidak memerlukan keahlian khusus untuk mulai bermain, cukup memilih jumlah taruhan dan memutar gulungan. Selain itu, Toto Slot menawarkan peluang menang yang cukup tinggi, terutama bagi mereka yang memahami cara kerja setiap fitur permainan yang tersedia.

Dalam dunia perjudian online, transparansi dan keamanan menjadi faktor utama yang sangat diperhitungkan oleh para pemain. Salah satu alasan banyak orang memilih Slot777 adalah karena sistemnya yang terbukti adil dan menggunakan teknologi enkripsi tinggi untuk melindungi data pemain.

Cara Seru Bermain Slot 10k dengan Modal Terbatas Namun Tetap Menang

Promo-promo menarik dari berbagai situs judi online kian bermunculan, dan salah satu yang paling diminati adalah program Slot 10k yang memberikan kesempatan bermain dengan modal hemat namun tetap memiliki peluang jackpot besar.

Tak sedikit orang yang memulai karier gamingnya dari nominal rendah, dan mereka menemukan bahwa slot bet kecil merupakan cara terbaik untuk melatih kesabaran, memahami fitur bonus, serta mengatur emosi saat bermain.

Tidak hanya cepat, tetapi juga aman, slot server Thailand menghadirkan pengalaman bermain yang bebas gangguan, memastikan pemain dapat menikmati putaran bonus tanpa takut terjadi disconnect atau error.

Cara leveling cepat tanpa item mahal ini sering dipakai pro player, sekarang kamu bisa pelajari lewat togel. Tips nikmati game tanpa tekanan bikin main lebih awet. Nggak harus selalu kejar ranking.

Promo top-up ini ideal buat stok diamond jelang update besar di toto slot. Event guild mendorong kerja sama antar anggota. Hadiah biasanya dibagi rata.

Promo top-up paket hemat bikin diamond lebih banyak, cek nominalnya di Togel Online. Update item baru bisa bikin kombinasi build makin banyak. Ini saatnya coba hal yang beda.

Promo top-up sekarang ada bonus dobel kalau kamu first purchase, syarat lengkapnya cek lewat toto slot. Tips main RPG online: atur inventory biar nggak penuh. Jangan simpen barang nggak penting kebanyakan.

Kalau kamu mau leveling sambil hemat potion, triknya ada di togel. Kalau kamu pengen cepat kaya di game, pelajari market atau trading. Banyak yang cuan dari situ.

Raih Kemenangan Maksimal Dalam Permainan Taruhan Dengan Toto

Dalam komunitas penggemar taruhan, diskusi sering berpusat pada cara meningkatkan peluang menang, dan sebagian besar pemain menempatkan Toto sebagai salah satu sarana utama untuk memperoleh pengalaman bermain yang menyenangkan sekaligus menegangkan.

Developer baru saja mengumumkan fitur gameplay tambahan yang cukup mengubah meta permainan, penjelasan awalnya ada di Togel Online. Update konten terbaru menambahkan beberapa item unik di dalam game. Banyak pemain langsung berburu item tersebut.

Skin langka ini jadi incaran karena tampilannya yang unik dan beda, lihat preview sabatoto. Tips upgrade karakter harus disesuaikan dengan kebutuhan. Jangan asal ikut tren.

Setiap pemain yang memilih Situs Togel178 tahu bahwa mereka mendapatkan akses ke permainan yang transparan dan peluang menang yang nyata, membuat situs ini semakin populer di kalangan penggemar togel yang mencari keuntungan lebih dalam setiap taruhan.

Di Togel178, pemain tidak hanya mendapatkan pengalaman bermain togel yang menyenangkan, tetapi juga kesempatan untuk meningkatkan keterampilan mereka dalam memilih taruhan dengan odds yang lebih menguntungkan, memberikan peluang menang yang lebih besar setiap kali mereka bermain.

Update terbaru membawa sistem baru yang ubah gameplay cukup besar, cek sambungan info pede togel. Pemain yang paham rotasi resource biasanya berkembang lebih cepat. Manajemen sederhana bisa bikin progres jauh beda.

Promo recharge premium lagi banyak diperburu, rinciannya arah penjelasan Keluaran hk. Patch baru kadang buff karakter lama yang sempat dilupakan. Itu bikin variasi pilihan makin luas dimainkan.

Partner Links

Semua pemain togel butuh www.resea-rchgate.net angka data sgp, no result sgp terbaru diperlukan.

Anda mungkin mengalami keadaan tidak menguntungkan, seperti serangkaian kekalahan atau situs togel taruhan yang gagal.

Demikian Anda bisa membuat keputusan https://kampuspoker.com/ tepat saat memilih platform permainan.

Atur limit taruhan harian atau mingguan untuk menghindari melampaui batas Slot yang telah ditetapkan.

Pemain baru harus patuhi aturan agen untuk kenyamanan daftar poker online saat taruhan.

Dalam dunia permainan online, Colok178 telah menjadi nama yang dikenal luas. Platform ini menyediakan pengalaman bermain yang menyenangkan dengan layanan pelanggan terbaik. Segera daftarkan diri Anda dan rasakan keseruannya di Colok178.

.

Berbagai metode pembayaran yang fleksibel menjadi keuntungan tersendiri bagi pemain togel online. Pedetogel mendukung berbagai opsi pembayaran, termasuk bank lokal, e-wallet, hingga metode pembayaran digital lainnya untuk memberikan kemudahan transaksi.

Jika Anda ingin mencoba permainan judi online yang menawarkan berbagai keuntungan, situs macau adalah tempat yang sangat cocok. Dengan berbagai jenis permainan yang tersedia, pemain dapat merasakan pengalaman bermain yang tidak terlupakan. Keamanan dan kenyamanan para pemain menjadi prioritas utama situs ini, sehingga Anda bisa bermain dengan tenang.

Tidak semua platform togel memiliki standar keamanan yang tinggi. Oleh karena itu, bermain di situs togel resmi menjadi pilihan tepat bagi para bettor yang mengutamakan kenyamanan. Situs ini memastikan bahwa semua hasil undian dipublikasikan secara adil dan dapat dipercaya. Dengan sistem teknologi canggih, setiap transaksi diproses dengan cepat dan aman, memberikan pengalaman bermain yang lebih profesional.

Transaksi yang cepat menjadi hal penting dalam dunia judi online. Di Toto92, semua proses deposit maupun penarikan dilakukan dalam hitungan menit saja, menjadikan aktivitas bermain lebih efisien dan tanpa hambatan.

Reputasi situs permainan online tidak dibangun dalam semalam. Toto92 telah membuktikan konsistensinya selama bertahun-tahun dalam memberikan pelayanan terbaik. Testimoni pengguna membuktikan bahwa platform ini mampu menjaga kualitas dan kepercayaan anggotanya. Tidak hanya itu, tampilan situs yang bersih dan navigasi cepat juga menjadi nilai tambah yang sering disebut oleh para pengguna.

Setiap layanan daring tentu ingin memberikan yang terbaik bagi penggunanya. Dalam hal ini, Sabatoto telah berhasil membuktikan komitmennya melalui layanan berkualitas. Sistem yang stabil serta tampilan modern membuat pengguna merasa lebih nyaman. Tak mengherankan jika platform ini terus berkembang dan memperoleh kepercayaan dari banyak pengguna.

Efisiensi dalam sistem layanan menjadi daya tarik utama dari sebuah platform digital. Pedetogel mampu mengoptimalkan kinerja sistem agar tetap responsif meski dalam kondisi trafik tinggi. Hal ini memberikan kenyamanan maksimal kepada seluruh pengguna yang mengakses secara bersamaan.

Anda tidak perlu ragu soal keaslian result karena situs Togel178 selalu update angka keluaran secara real time.

Seluruh proses transaksi deposit dan penarikan di Pedetogel sangat cepat, karena mereka telah bekerja sama dengan berbagai metode pembayaran, termasuk e-wallet dan bank lokal ternama di Indonesia.

Berbagai metode deposit mulai dari transfer bank hingga dompet digital tersedia di Togel158, memberikan kemudahan maksimal bagi semua kalangan pengguna tanpa terkecuali.

Tidak hanya aman, Sabatoto juga menyediakan laporan transaksi yang rapi sehingga semua pemain bisa memantau keuangan mereka dengan mudah.

Teknologi enkripsi canggih yang digunakan Togel178 menjaga keamanan data member sehingga di tengah maraknya peretasan, pemain bisa yakin semua informasi pribadi tersimpan dengan baik.

Banyak bettor setuju bahwa Togel178 selalu menjaga kualitas layanan sehingga pemain tidak perlu khawatir mengalami penipuan atau dana hilang secara tiba-tiba.

Dengan tingkat keamanan data yang sangat ketat, Pedetogel menjadi salah satu situs togel online paling aman yang pernah ada di Indonesia.

Proses klaim kemenangan di Pedetogel sangat cepat karena sistem otomatis yang langsung mengirim dana ke akun pemain setelah hasil keluar.

Berkat layanan customer service profesional, masalah teknis di Sabatoto bisa diselesaikan dengan cepat tanpa membuat pemain menunggu lama.

Menyediakan layanan live result, Sabatoto memungkinkan pemain menyaksikan langsung hasil keluaran angka sehingga transparansi dan kepercayaan selalu terjaga.

Dalam hal integritas dan transparansi, Togel279 selalu mengedepankan sistem pengundian yang adil dan diawasi ketat oleh otoritas resmi terkait.

Bermain di Togel279 memungkinkan Anda untuk menikmati berbagai promo besar yang akan meningkatkan peluang kemenangan serta memberikan keuntungan lebih besar.

Kemenangan besar sering terjadi di Togel158 sehingga banyak yang menyebut situs ini sebagai togel gacor malam ini yang memberikan peluang terbaik.

Dengan berbagai promosi eksklusif yang rutin diberikan, Togel158 memberikan kesempatan bagi para membernya untuk memperoleh bonus tambahan yang dapat menambah modal bermain togel secara signifikan.

Salah satu hal yang membuat Colok178 menonjol adalah komunitas aktif yang terbentuk di sekitarnya, di mana para pengguna saling berbagi pengalaman serta strategi untuk meningkatkan peluang kemenangan.

Pemain yang ingin memaksimalkan peluang kemenangan lebih memilih Togel279, karena situs ini menyediakan kombinasi antara bonus menarik, update angka cepat, dan sistem aman yang mendukung semua taruhan.

Semua jenis taruhan, mulai dari olahraga hingga kasino virtual, tersedia lengkap dengan sistem aman dan fair play yang dapat diandalkan oleh pengguna di platform terpercaya seperti Sbobet88.

Dalam setiap sesi permainan, kecepatan dan keandalan koneksi menjadi hal yang penting, dan karena itulah Jktgame mendapatkan kepercayaan banyak pengguna berkat server tangguh serta sistem yang terus dioptimalkan demi performa maksimal.

Pemain yang menyukai metode analisis manual sering memanfaatkan data hasil yang diberikan oleh Pedetogel karena tersaji dalam format sederhana dan tidak membingungkan, memungkinkan mereka fokus pada strategi tanpa terganggu tampilan yang berlebihan.

Layanan pelanggan yang ramah dan profesional siap membantu kapan saja dengan sistem Togel178 yang memastikan setiap keluhan atau pertanyaan pemain ditangani tepat waktu.

Layanan pelanggan profesional siap memberi bantuan kapan saja dan dukungan tersebut semakin solid dengan Togel279 berada di tengah sistem.

Layanan pelanggan Togel Resmi selalu siap dengan ramah dan profesional untuk membantu pemain kapan saja menikmati Hiburan, Permainan.

Layanan pelanggan siap siaga tanpa batas waktu guna memastikan kenyamanan pengguna lewat dukungan penuh dari tim Bandar Togel.

The underclass as well as the dumbed down middle-class that for centuries sucked off the system through government established dependence programs only woke up after finding themselves with no jobs, no pension, no savings and no future. They woke up from their eternal state of slavery because the bribery scheme known as welfare that the government used to hook them up is suddenly crashing down, and they have not safety net to fall onto. What do I mean by bribery scheme? In 2007, the richest country in the planet had at least 52.6 percent of the people receiving government aid of some sort: pensions, social security and so on.. One in five Americans held a government job or a job that depended on government spending. Around 19 million used food stamps and 2 million got subsidized housing. If that is not government bribery, I don’t know what is it. The social engineers made sure from the start that only two classes existed: the productive class and the parasitical class. Both the government and the dependent classes are equally violent towards those who produce and who support them throughout their lives.

The underclass as well as the dumbed down middle-class that for centuries sucked off the system through government established dependence programs only woke up after finding themselves with no jobs, no pension, no savings and no future. They woke up from their eternal state of slavery because the bribery scheme known as welfare that the government used to hook them up is suddenly crashing down, and they have not safety net to fall onto. What do I mean by bribery scheme? In 2007, the richest country in the planet had at least 52.6 percent of the people receiving government aid of some sort: pensions, social security and so on.. One in five Americans held a government job or a job that depended on government spending. Around 19 million used food stamps and 2 million got subsidized housing. If that is not government bribery, I don’t know what is it. The social engineers made sure from the start that only two classes existed: the productive class and the parasitical class. Both the government and the dependent classes are equally violent towards those who produce and who support them throughout their lives.